Fundamental Strength Indicator Final w/ Weighting

Source code

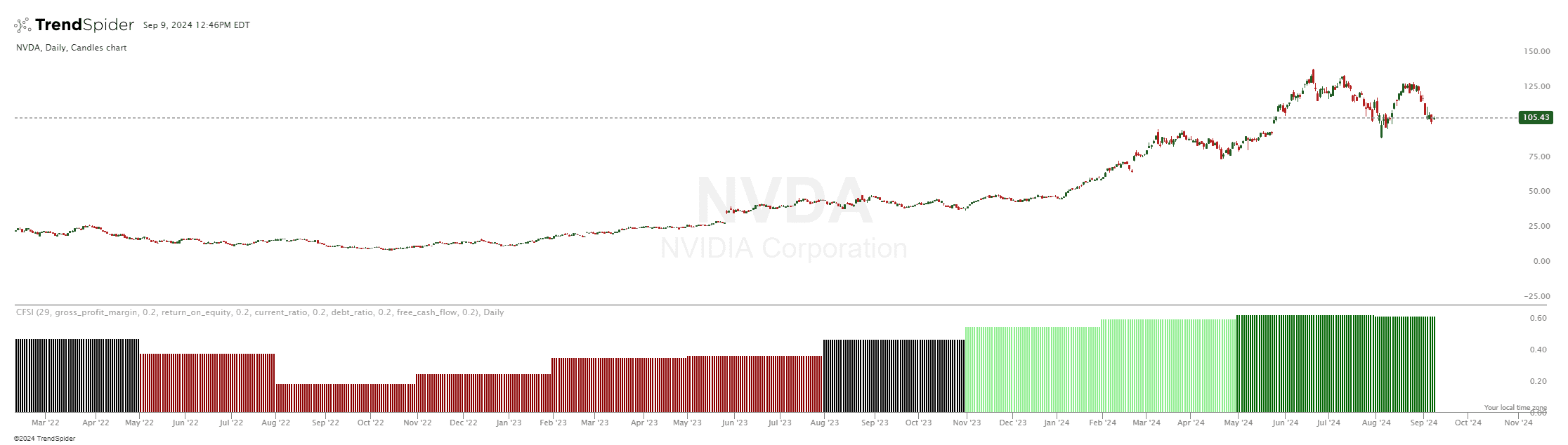

This indicator had been implemented by James in JavaScript on TrendSpider. Check out the developer documentation to learn more about JS on TrendSpider.

// This indicator code was potentially generated using AI. It was not checked by Quality Assurance

// and did not pass any quality assurance processes that we normally would use at TrendSpider

// As a result, I can’t guarantee that it will operate as expected in all cases and you should

// use caution when using this indicator. Consider it for informational purposes only.

// testing testing

// Import necessary libraries

const moment = library('moment-timezone');

// Declare the indicator with a user-friendly name and type

describe_indicator('Fundamental Strength Indicator Final w/ Weighting', 'lower', {

shortName: 'CFSI',

decimals: 2

});

// Input parameters for the number of quarters to fetch

const quarters = input('Number of Quarters', 29);

const metric1 = input('Metric 1', 'gross_profit_margin', [

'gross_profit_margin', 'return_on_equity', 'current_ratio', 'debt_ratio', 'free_cash_flow',

'net_income', 'operating_margin', 'revenue', 'ebitda', 'fcf_to_net_income',

'book_to_market_value', 'cash_cash_equivalents', 'debt_to_equity_ratio', 'net_profit_margin',

'total_assets', 'total_equity', 'total_liabilities', 'pretax_income_loss_adj',

'net_income_discontinued_operations', 'eps_diluted'

]);

const weight1 = input('Weight 1', 0.2, { min: 0, max: 1, step: 0.01 });

const metric2 = input('Metric 2', 'return_on_equity', [

'gross_profit_margin', 'return_on_equity', 'current_ratio', 'debt_ratio', 'free_cash_flow',

'net_income', 'operating_margin', 'revenue', 'ebitda', 'fcf_to_net_income',

'book_to_market_value', 'cash_cash_equivalents', 'debt_to_equity_ratio', 'net_profit_margin',

'total_assets', 'total_equity', 'total_liabilities', 'pretax_income_loss_adj',

'net_income_discontinued_operations', 'eps_diluted'

]);

const weight2 = input('Weight 2', 0.2, { min: 0, max: 1, step: 0.01 });

const metric3 = input('Metric 3', 'current_ratio', [

'gross_profit_margin', 'return_on_equity', 'current_ratio', 'debt_ratio', 'free_cash_flow',

'net_income', 'operating_margin', 'revenue', 'ebitda', 'fcf_to_net_income',

'book_to_market_value', 'cash_cash_equivalents', 'debt_to_equity_ratio', 'net_profit_margin',

'total_assets', 'total_equity', 'total_liabilities', 'pretax_income_loss_adj',

'net_income_discontinued_operations', 'eps_diluted'

]);

const weight3 = input('Weight 3', 0.2, { min: 0, max: 1, step: 0.01 });

const metric4 = input('Metric 4', 'debt_ratio', [

'gross_profit_margin', 'return_on_equity', 'current_ratio', 'debt_ratio', 'free_cash_flow',

'net_income', 'operating_margin', 'revenue', 'ebitda', 'fcf_to_net_income',

'book_to_market_value', 'cash_cash_equivalents', 'debt_to_equity_ratio', 'net_profit_margin',

'total_assets', 'total_equity', 'total_liabilities', 'pretax_income_loss_adj',

'net_income_discontinued_operations', 'eps_diluted'

]);

const weight4 = input('Weight 4', 0.2, { min: 0, max: 1, step: 0.01 });

const metric5 = input('Metric 5', 'free_cash_flow', [

'gross_profit_margin', 'return_on_equity', 'current_ratio', 'debt_ratio', 'free_cash_flow',

'net_income', 'operating_margin', 'revenue', 'ebitda', 'fcf_to_net_income',

'book_to_market_value', 'cash_cash_equivalents', 'debt_to_equity_ratio', 'net_profit_margin',

'total_assets', 'total_equity', 'total_liabilities', 'pretax_income_loss_adj',

'net_income_discontinued_operations', 'eps_diluted'

]);

const weight5 = input('Weight 5', 0.2, { min: 0, max: 1, step: 0.01 });

const metrics = [metric1, metric2, metric3, metric4, metric5];

const weights = [weight1, weight2, weight3, weight4, weight5];

// Fetch fundamental data for the ticker

const ticker = current.ticker;

const fundamentalData = await request.fundamental(ticker, metrics, quarters);

assert(!fundamentalData.error, `Error fetching fundamental data: ${fundamentalData.error}`);

// Extract fundamental metrics and their timestamps

function getMetricData(data, metric) {

return data[metric].map(dp => ({ value: dp.value, timestamp: dp.reportdate }));

}

// Normalize the data between 0 and 1

function normalize(data) {

const values = data.map(d => d.value);

const min = Math.min(...values);

const max = Math.max(...values);

return data.map(d => ({ ...d, value: (d.value - min) / (max - min) }));

}

// Create series for each selected metric

const metricSeries = {};

metrics.forEach((metric, index) => {

const data = getMetricData(fundamentalData, metric);

const normalizedData = normalize(data);

metricSeries[`metric${index + 1}`] = series_of(null);

for (let i = 0; i < time.length; i++) {

const currentTimestamp = time[i];

const value = normalizedData.find(d => d.timestamp <= currentTimestamp);

metricSeries[`metric${index + 1}`][i] = value ? value.value : null;

}

});

// Create series for the composite score over time

const compositeScoreSeries = series_of(null);

const compositeScoreColors = series_of(null);

for (let i = 0; i < time.length; i++) {

const scores = metrics.map((metric, index) => metricSeries[`metric${index + 1}`][i]);

if (scores.every(score => score !== null)) {

const compositeScore = scores.reduce((acc, score, index) => acc + score * weights[index], 0);

compositeScoreSeries[i] = compositeScore;

compositeScoreColors[i] = compositeScore > 0.6 ? 'darkgreen' : compositeScore > 0.5 ? 'lightgreen' : compositeScore > 0.4 ? 'lightred' : 'darkred';

} else {

compositeScoreSeries[i] = null;

compositeScoreColors[i] = null;

}

}

// Paint the indicator on the chart as a histogram with colors

paint(compositeScoreSeries, {

name: 'Fundamental Strength Indicator',

color: compositeScoreColors,

thickness: 2,

style: 'column'

});

Automated technical analysis software. For traders, by traders.